Hot Topics:

- Dolar Index closes bearish helped by mixed CPI data.

- EUR-USD is losing momentum.

- Manufacturing Production (YoY) falls, and pound closes slightly upward.

- BoJ – Kuroda keeps the promise of monetary policy.

- Crude Oil climbs to the highest level since 2014.

Dolar Index closes bearish helped by mixed CPI data.

The index of the greenback yesterday closed down 0.04%, finding support at level 89.03 weighed down by mixed inflation data. On the one hand, Core CPI (YoY) rose to 2.1% in March from 1.8% registered in February. On the other side, the Consumer Price Index CPI (MoM) fell to -0.1% in March, while in February it recorded an advance of 0.2%. We continue to observe the lateral range in which the price is with a bearish bias. (Click on the chart for full resolution).

EUR-USD is losing momentum.

The pair of the single currency is losing momentum, in the fourth consecutive trading session, the euro advanced 0.10% finding resistance at 1.2395. In an interview with Reuters, the ECB lawmaker Ardo Hansson said that the ECB “needs to be patient and eliminate its stimulus very gradually.”

Although the ECB has kept the interest rate at low levels and has maintained its policy of buying bonds, lawmakers are debating that it is time to start cutting this policy. ECB legislator Ewald Nowotny, meanwhile, said he would have “no problem” in raising the deposit rate from -0.4% to -0.2% as a means to normalise monetary policy.

In this macroeconomic context, the euro is reaching a key area in the range 1.2412 – 1.245. Should not exceed the level 1.2476, the pair could make a new bearish leg. In the long term, we still have our eyes on 1.26 as the end zone of the EUR / USD bullish cycle.

Manufacturing Production (YoY) falls, and pound closes slightly upward.

Manufacturing Production (YoY) fell to 2.5% in February well below the consensus that estimated an advance of 3.3%. The sector that was most affected was the construction sector with a decline of 1.6% in February. The National Statistics Office attributes to a large extent these low figures to the effect of severe weather.

On the technical side, we are observing a possible corrective process that could begin to be developed from area 1.42 – 1.425 with a potential level of invalidation in over 1.4345 coinciding with the highest level of the year.

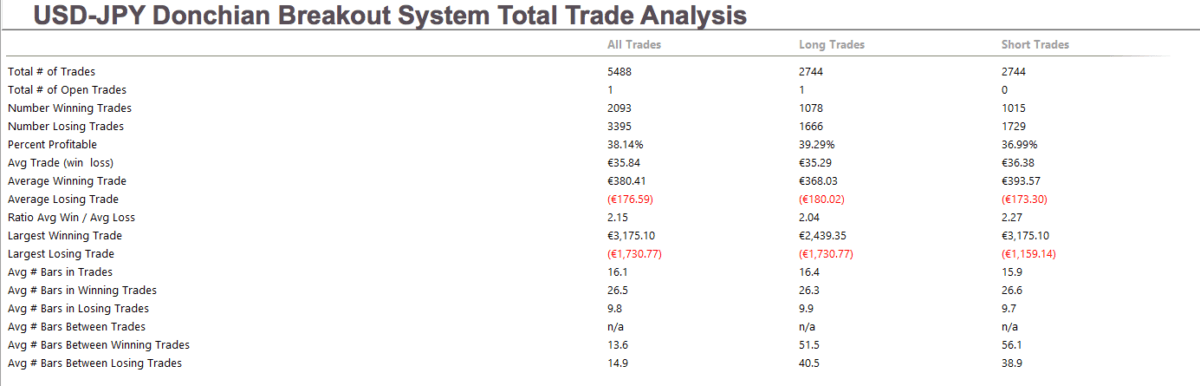

BoJ – Kuroda keeps the promise of monetary policy.

The Governor of the Bank of Japan, Haruhiko Kuroda, reiterated his optimistic view on the expansion of Japan’s economy, affirming that “With the improvement of the product gap and the medium to long-term inflation expectations observed, we expect that inflation will accelerate as a trend and go to 2 percent. ”

On a technical level, on the one hand, the USD-JPY is still in a limited lateral range between 106.64 and 107.49, the predominant bias is bullish and increases its probability of strength as it closes above 108. The level The invalidation of the bullish sequence is 105.66.

On the other hand, by a positive correlation concerning USDJPY, we see in the Nikkei 225 Index within a long-term bearish pattern developing an ascending diagonal formation, which in case of exceeding 21,957 could lead to exceeding 22,500 pts.

Crude Oil climbs to the highest level since 2014.

First, it was the turn of the Brent oil; now it is the turn of the Crude oil that has climbed to the highest levels since 2014, reaching 67.36 US $ / Barrel, while the Brent oil climbed to new highs reaching $72.69.

For the Brent Oil, although the trend is bullish, the closest resistance is $72.91, while the level of invalidation of the bullish cycle is below $67.

As with the Brent Oil, the Crude Oil is in a free climb up to $ 70.7 as long as it remains above the $64 level.

On the opposite side, by inverse correlation, the Loonie remains in free fall with a target at the base of the bullish channel, the impact zone could be between 1.2456 to 1.235.