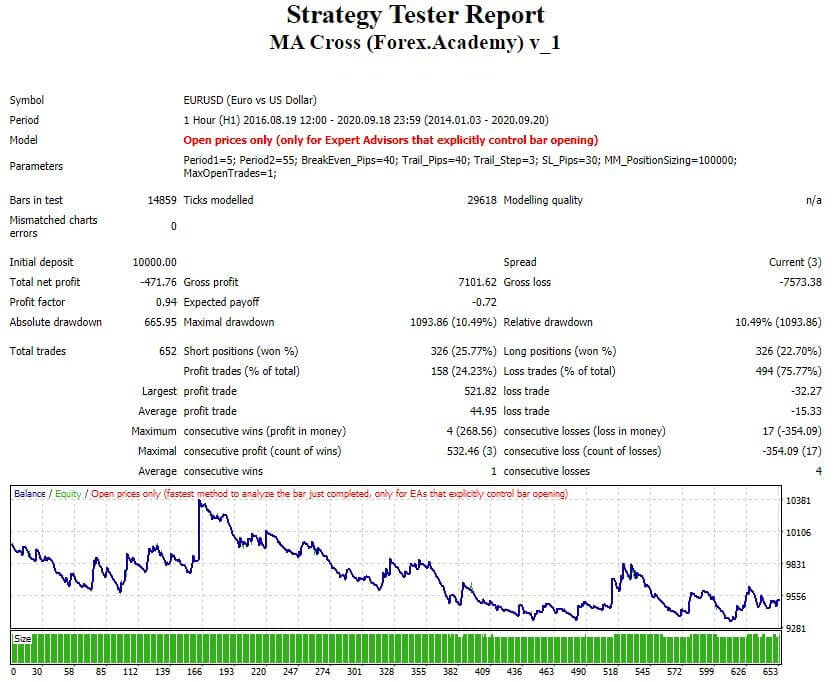

Trading the naked RSI system depicted in this series’s previous video as an overbought/oversold signal generator is too risky, and its long-term results questionable. The system is profitable only in sideways movements. Thus, a trending filter or a detrending step will be needed to avoid the numerous fake signals.

Divergences and Failure swings

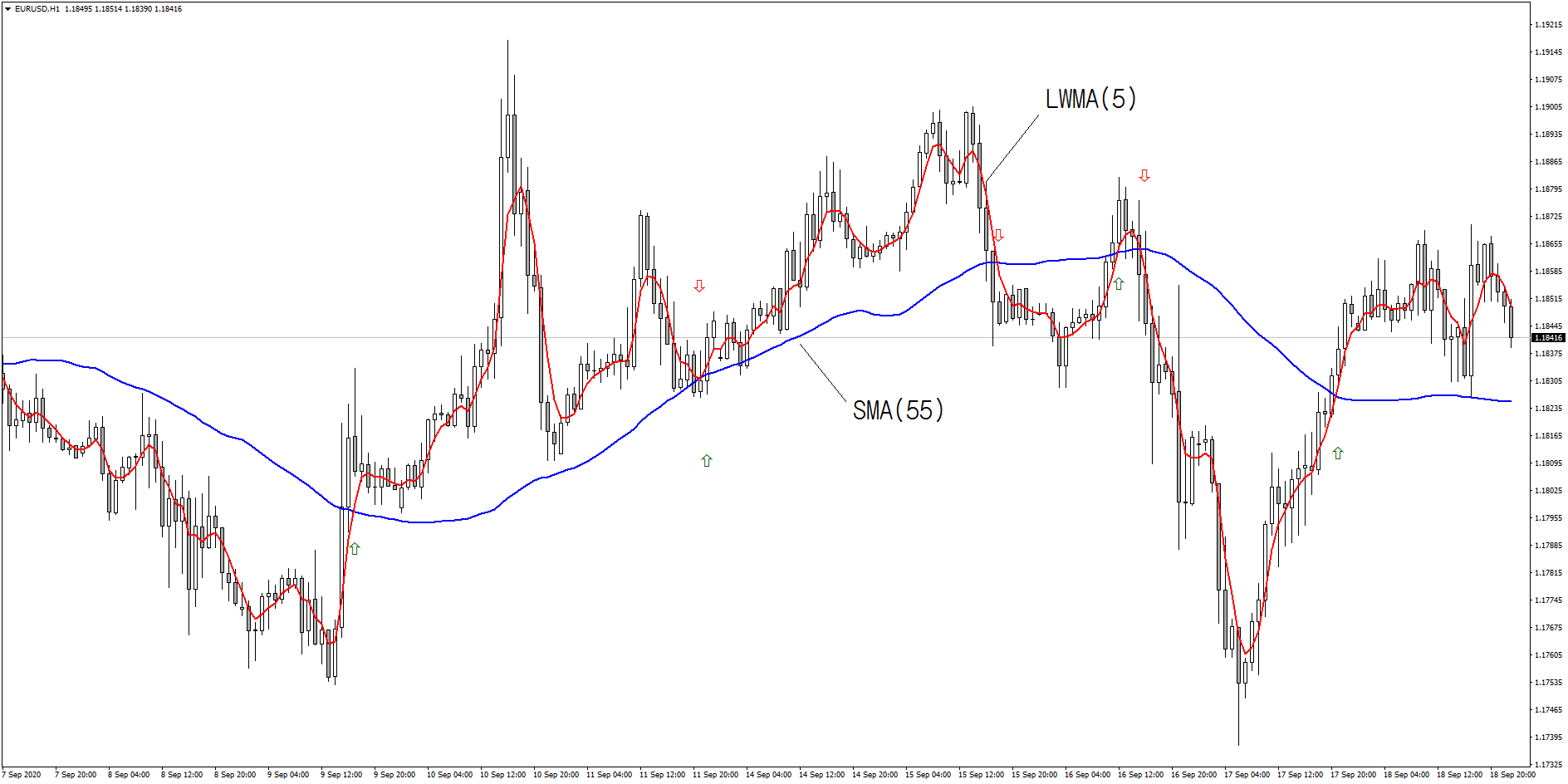

Welles Wilder remarks on two ways to trade the RSI: Divergences and Top/Bottom failure swings.

Divergences

A divergence forms when the price makes higher highs (or lower lows), and the RSI makes the opposite move: lower highs (or higher lows). RSI divergences from the oversold area show the market action starts to strengthen, an indication of a potential swing up. In contrast, RSI divergences in the overbought area show weakness and a likely retracement from the current upward movement.

Failures

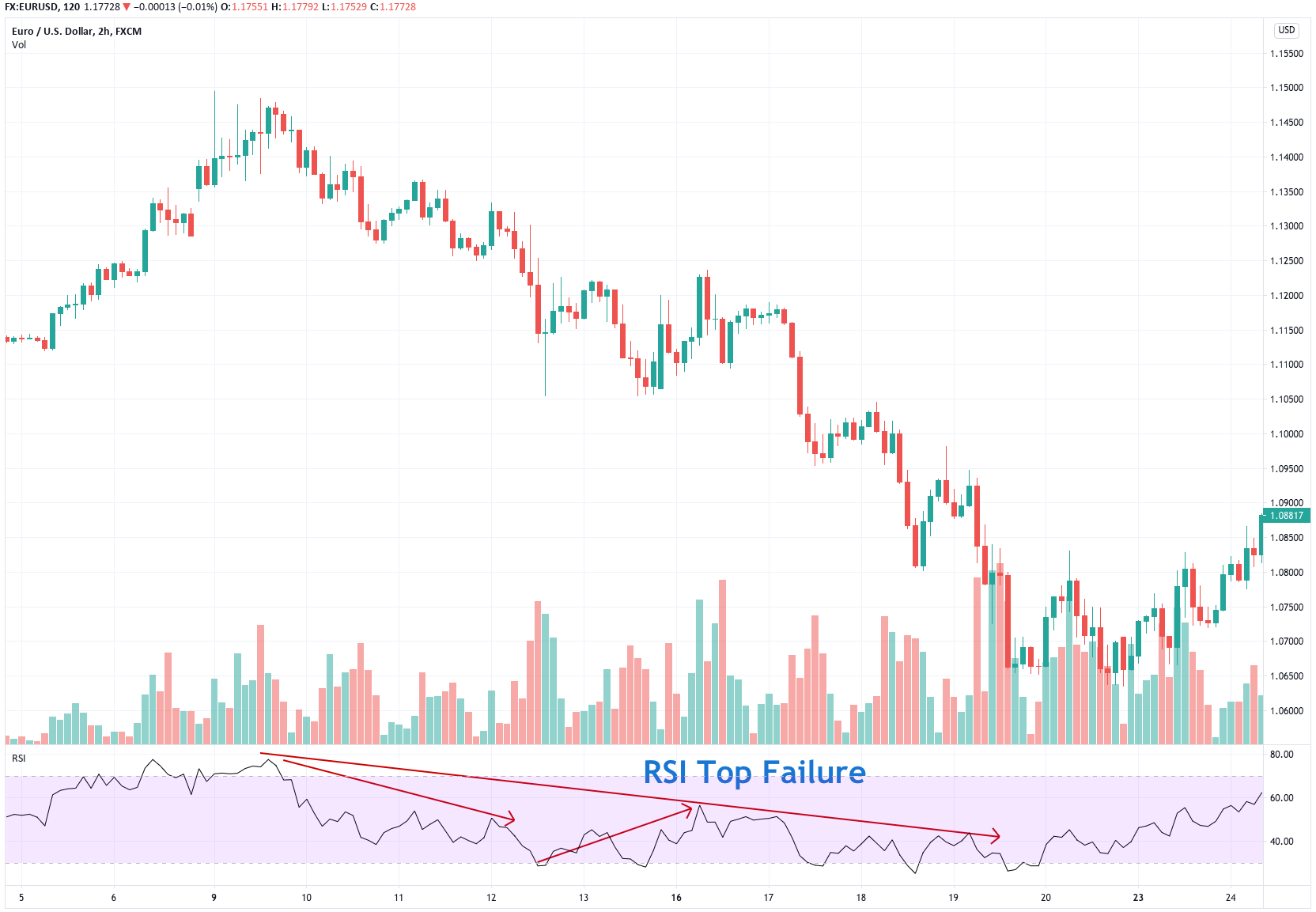

An RSI Top failure occurs with the following sequence of events:

- The RSI forms a pivot high in the overbought area.

- An RSI pullback occurs, and an RSI pivot low forms.

- A new RSI pivot high forms, which is lower than the previous pivot high

Fig 1 – RSI TOP failures in the EURUSD 4H 2H Chart

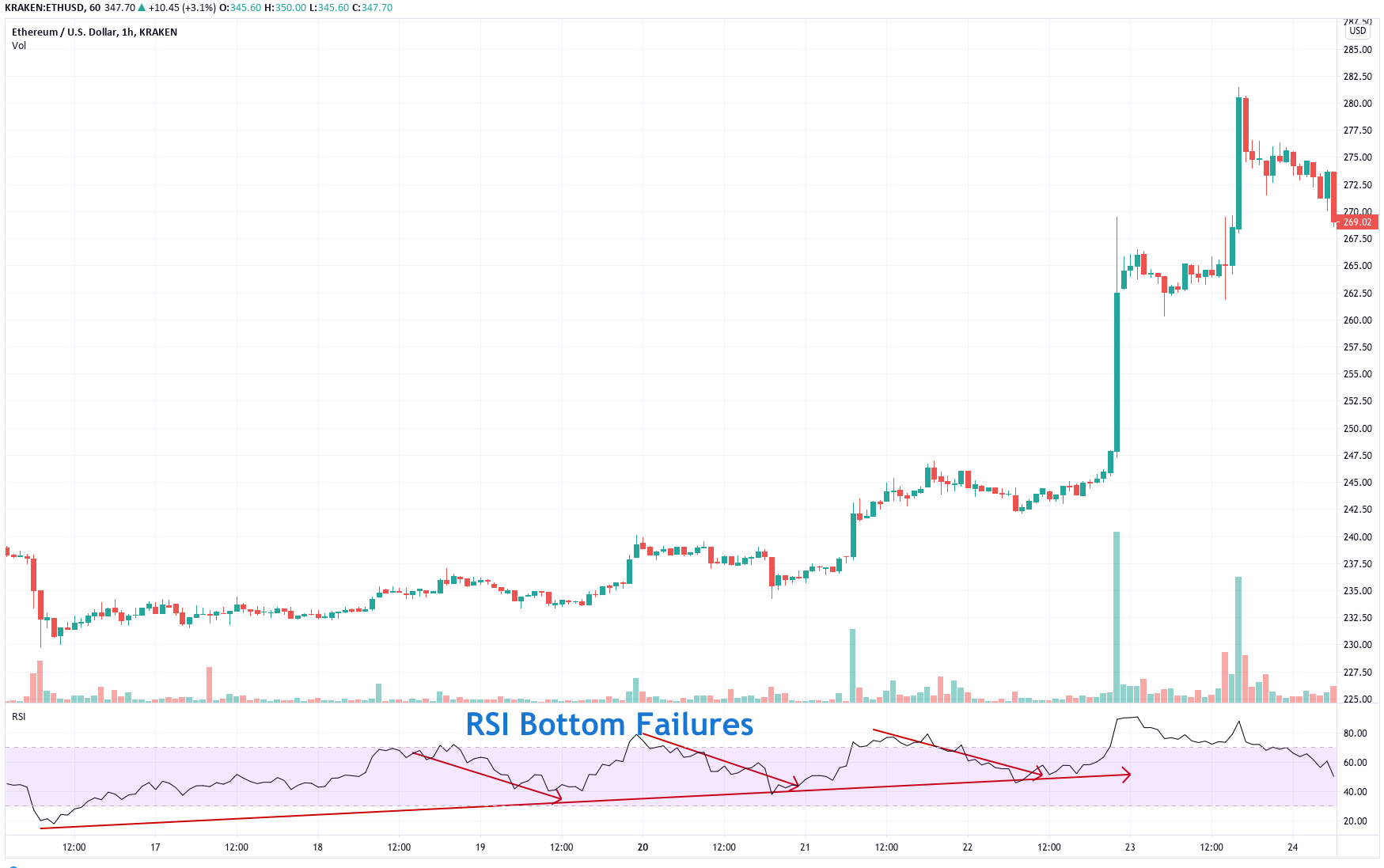

An RSI Bottom failure occurs with the following sequence of events:

- The RSI forms a pivot low below the oversold area.

- An RSI pullback occurs, and an RSI pivot high forms.

- A new RSI pivot low forms, which is higher than the previous pivot high.

Fig 2 – RSI Bottom failures in the ETHUSD 1H Chart.

Fig 2 – RSI Bottom failures in the ETHUSD 1H Chart.

According to Welles Wilder, trading the RSI failure swings can be more profitable than trading the RSI overbought-oversold system. Thus, we will test it.

The RSI Failure algorithm

To create the RSI Failure algorithm, we will need to use the Finite State Machine concept, presented in this series’s seventh video.

The Easylanguage code of the RSI system failure is the following:

inputs: Price( Close ), Length( 14 ), OverSold( 30 ), Overbought( 70 ),

takeprofit( 3 ), stoploss( 1 ) ;

variables: state(0), state1 (0), state2(0), state5 (0), state6(0), rsiValue(0),

var0( 0 ), rsi_Pivot_Hi(0), rsiPivotHiFound(False),

rsiPivotLoFound (False),rsi_Pivot_Lo(0) ;

rsiValue = RSI(C,Length);

If rsiValue[1] > rsiValue and rsiValue[1] > rsiValue[2] then

begin

rsiPivotHiFound = true;

rsi_Pivot_Hi= rsiValue[1];

end

else

rsiPivotHiFound = False;

If rsiValue[1] < rsiValue and rsiValue[1] < rsiValue[2] then

begin

rsiPivotLoFound = true;

rsi_Pivot_Lo = rsiValue[1];

end

else

rsiPivotLoFound = False;

If state = 0 then

begin

if rsiPivotHiFound = true and rsi_Pivot_Hi> Overbought then

state = 1 {a bearih setup begins}

else

if rsiPivotLoFound = True and rsi_Pivot_Lo < OverSold then

state = 5; {a bullish Setup begins}

end;

{The Bearish setup}

If state = 1 then

begin

state1 = rsi_Pivot_Hi;

if rsiValue > state1 then state = 0;

if rsiPivotLoFound = true then

state = 2;

end;

If state = 2 then

begin

state2 = rsi_Pivot_Lo ;

if rsiValue > state1 then state = 0;

if rsiPivotHiFound = true then

if rsi_Pivot_Hi< 70 then state = 3;

end;

If state = 3 then

if rsiValue < state2 then state = 4;

If state = 4 then

begin

sellShort this bar on close;

state = 0;

end;

{The bullish setup}

If state = 5 then

begin

state5 = rsi_Pivot_Lo;

if rsiValue < state5 then state = 0;

if rsiPivotHiFound = true then

state = 6;

end;

If state = 6 then

begin

state6 = rsi_Pivot_Hi;

if rsiValue < state5 then state = 0;

if rsiPivotLoFound = true then

if rsi_Pivot_Lo > OverSold then state = 7;

end;

If state = 7 then

if rsiValue > state6 then state = 8;

If state = 8 then

begin

buy this bar on close;

state = 0;

end;

If state > 0 and rsiValue < OverSold then state = 0;

If state > 0 and rsiValue > Overbought then state = 0;

{The Long position management section}

If marketPosition =1 and close < entryprice - stoploss* avgTrueRange(10) then

sell this bar on close;

If marketPosition =1 and close < entryPrice + takeprofit* avgTrueRange(10) then

sell this bar on close;

{The Short position management section}

If marketPosition =-1 and close > entryprice + stoploss* avgTrueRange(10) then

BuyToCover this bar on close;

If marketPosition =-1 and close < entryPrice - takeprofit* avgTrueRange(10) then

BuyToCover this bar on close;

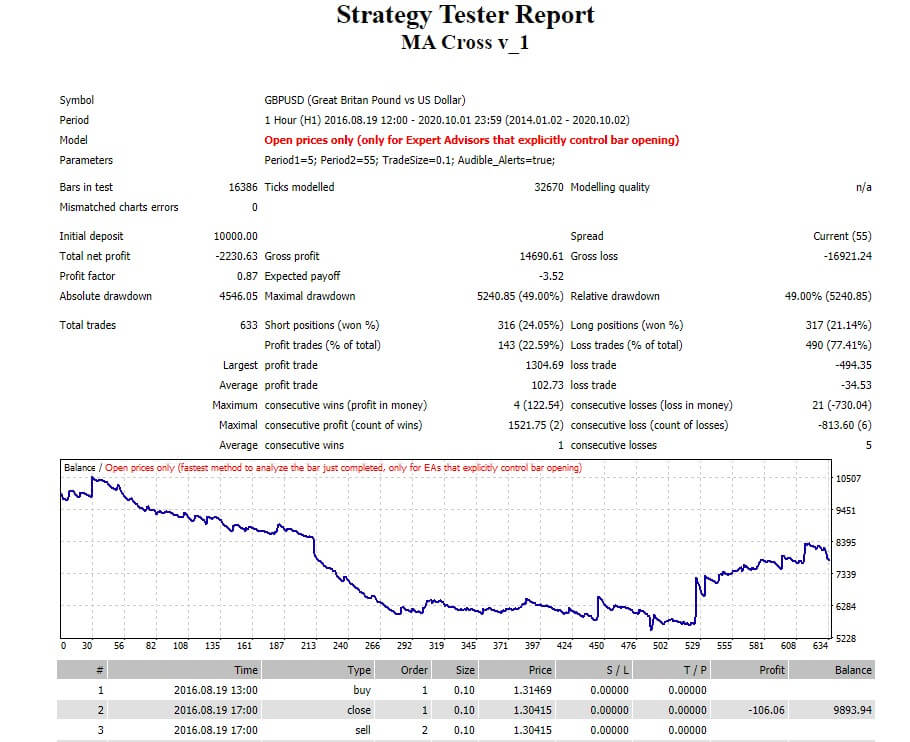

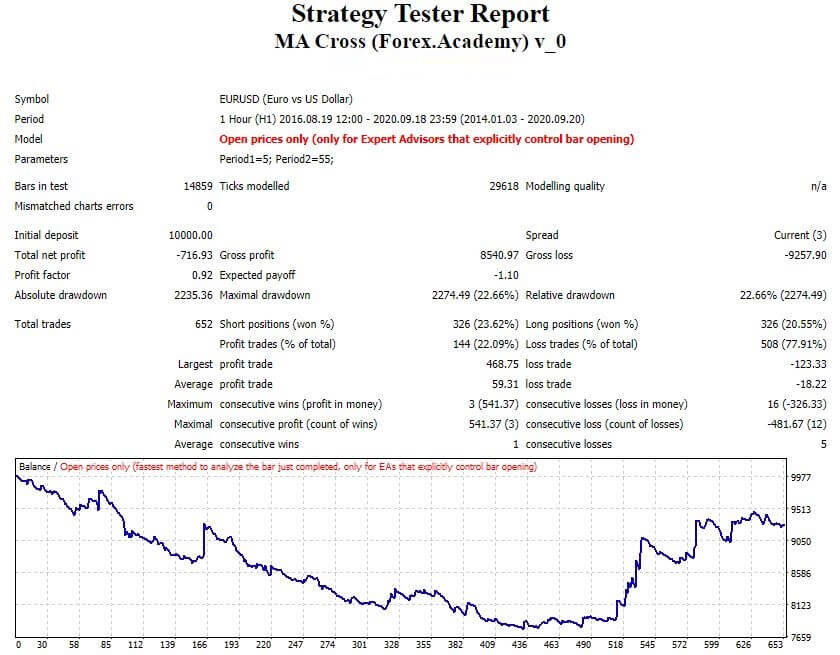

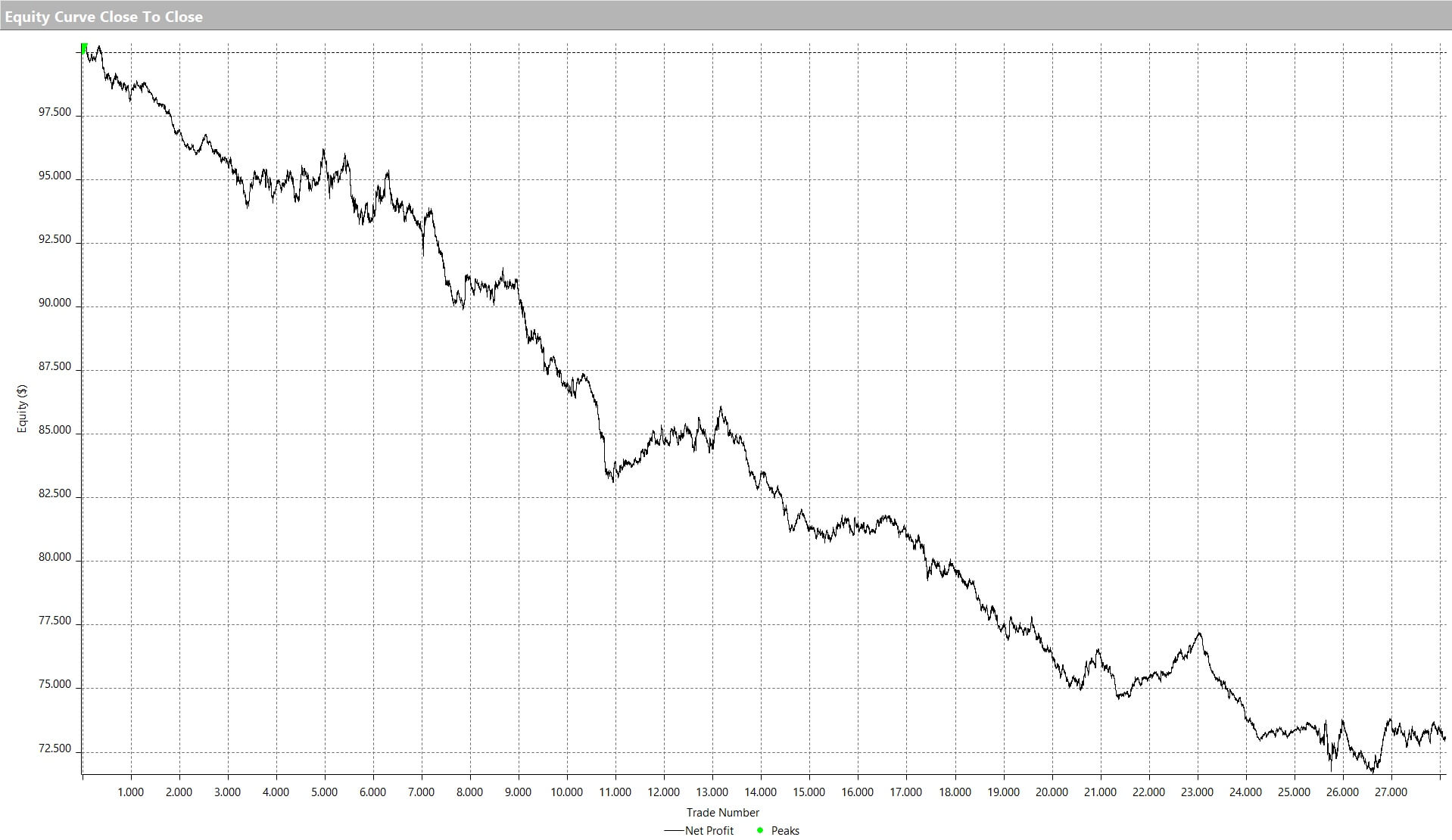

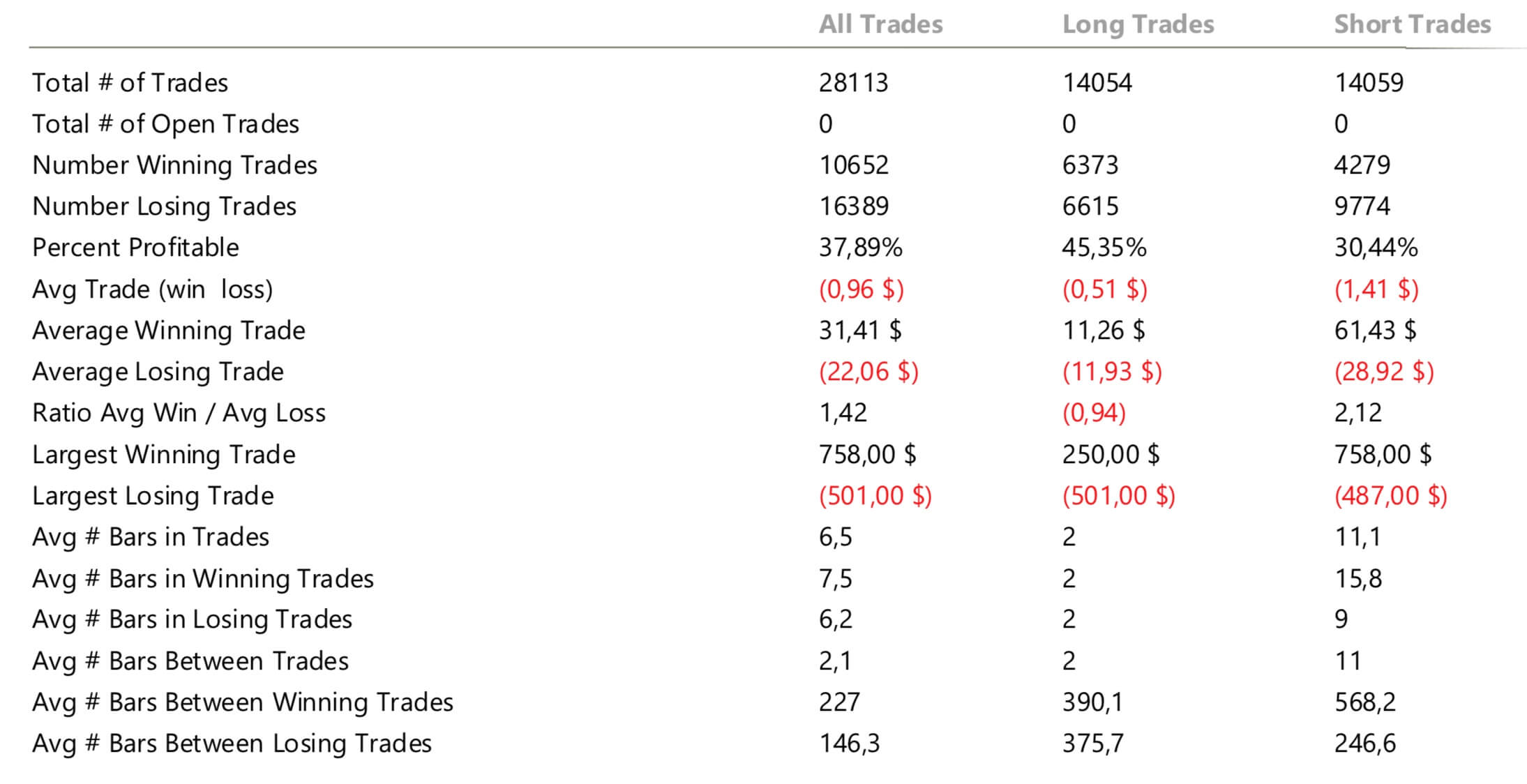

The results, measured on the EURUSD, are not as brilliant as Mr. Welles Wilder stated.

The trade analysis shows that the RSI Failures system, as is, is a losing system. This fact is quite common. It takes time to uncover good ideas for a profitable trading system. In the meantime, we have developed a practical exercise using the finite state machine concept, handy for the future development of our own trading ideas.

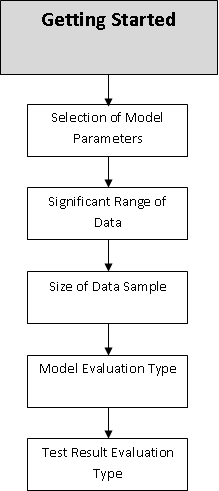

As said in our previous video, financial markets are unbounded territories where each trader needs to set his own rules; otherwise, they will be influenced by his emotions and fail. A trading system is their set of rules that enable them a long-term success.

As said in our previous video, financial markets are unbounded territories where each trader needs to set his own rules; otherwise, they will be influenced by his emotions and fail. A trading system is their set of rules that enable them a long-term success. The chosen timeframe should match the availability to trade. A trader with a day job would need to select a daily or a 12-hour timeframe, whereas a full-time trader could use shorter frames, such as 15-min, one, two, or four-hour timeframes.

The chosen timeframe should match the availability to trade. A trader with a day job would need to select a daily or a 12-hour timeframe, whereas a full-time trader could use shorter frames, such as 15-min, one, two, or four-hour timeframes. A permisioning filter is a way to avoid trading under determined circumstances. It can be a filter that allows only trading in the direction of the primary trend or an overbought/oversold sign that should be on for a determined candlestick or pattern formation to be valid.

A permisioning filter is a way to avoid trading under determined circumstances. It can be a filter that allows only trading in the direction of the primary trend or an overbought/oversold sign that should be on for a determined candlestick or pattern formation to be valid.

Position sizing is the part of your plan that tells you how much risk you should take on a trade. We have had a

Position sizing is the part of your plan that tells you how much risk you should take on a trade. We have had a