In part 1 of this article series, we have created the Stochastic RSI indicator as part of our idea for a scalping strategy. Now that we have it functional, we will make the bull/bear phases and visually inspect whether it captures the turning market’s turning points.

Possible ways to create bull/bear slices

Our Stochastic RSI consists of two lines, k and d, and two trigger lines, ob and os. Therefore we can use multiple variants that may allow the creation of bull/bear price legs. Let’s consider the following 3

Variant 1 – The transition occurs at the SRSI entrance of the oversold or overbought regions.

Bull: The d-line crosses under the ob-line, which indicates it is into the overbought area

Bear: The d-line crosses over the os-line, indicating d‘s entry into the oversold area.

Code:

if crossunder (d, os)

SRSI_Long := true

SRSI_Short := false

else if crossover (d, ob)

SRSI_Long := false

SRSI_Short := true

else

SRSI_Long := SRSI_Long[1]

SRSI_Short := SRSI_Short[1]

This code creates a condition SRSI_Long at the cross of d under os, which holds until d crosses over ob and reverses it, creating an SRSI_Short state. This condition is only modified by d crossing under os.

The else statement ensures the condition does not change from the previous bar.

Once we have defined the bull and bear segments, we can color-shade them to visualize them in the chart. To do it, we will use the bgcolor() function.

bgcolor(SRSI_Long ? color.green: na) bgcolor(SRSI_Short ? color.red: na)

The first statement asks the condition of SRI-Long ( the ? sign). If true, the background color changes to green. Otherwise, no change (an). The second statement behaves similarly for SRSI_Short.

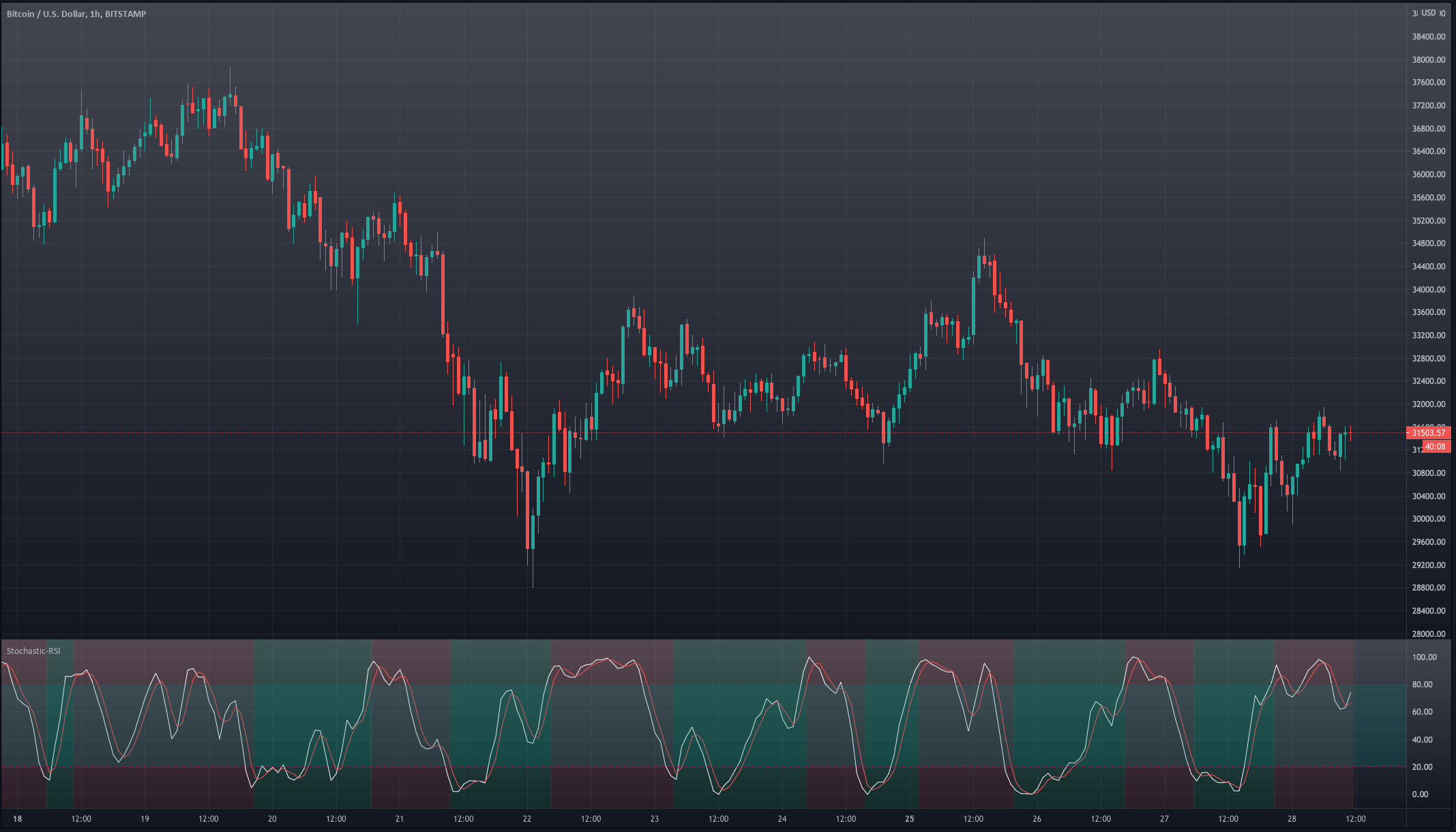

Let’s see how this piece of code behaves in the BTCUSD chart.

Variant 1 triggers the transitions too early. We see that on many occasions when the stochastic RSI enters the overbought or oversold region, it is more a signal of trend strength than a turning point.

Variant 1 triggers the transitions too early. We see that on many occasions when the stochastic RSI enters the overbought or oversold region, it is more a signal of trend strength than a turning point.

Variant 2 – The transition occurs at D and K’s crossovers if in the overbought/oversold regions.

Bull: the k-line crosses over the d-line, if below os ( inside the oversold region. We ignore crosses in the mid-area)

Bear: the k-line crosses under the d-line, if above ob ( in the overbought area. We ignore crosses in the mid-area)

Code:

// creating the long and short conditions for case 2

if crossover(k,d) and d < os SRSI_Long := true SRSI_Short := false else if crossunder(k,d) and d > ob SRSI_Long := false SRSI_Short := true else SRSI_Long := SRSI_Long[1] SRSI_Short := SRSI_Short[1] // bacground color change bgcolor(SRSI_Long ? color.green: na) bgcolor(SRSI_Short ? color.red: na)

The last section for the background change is similar to Variant 1.

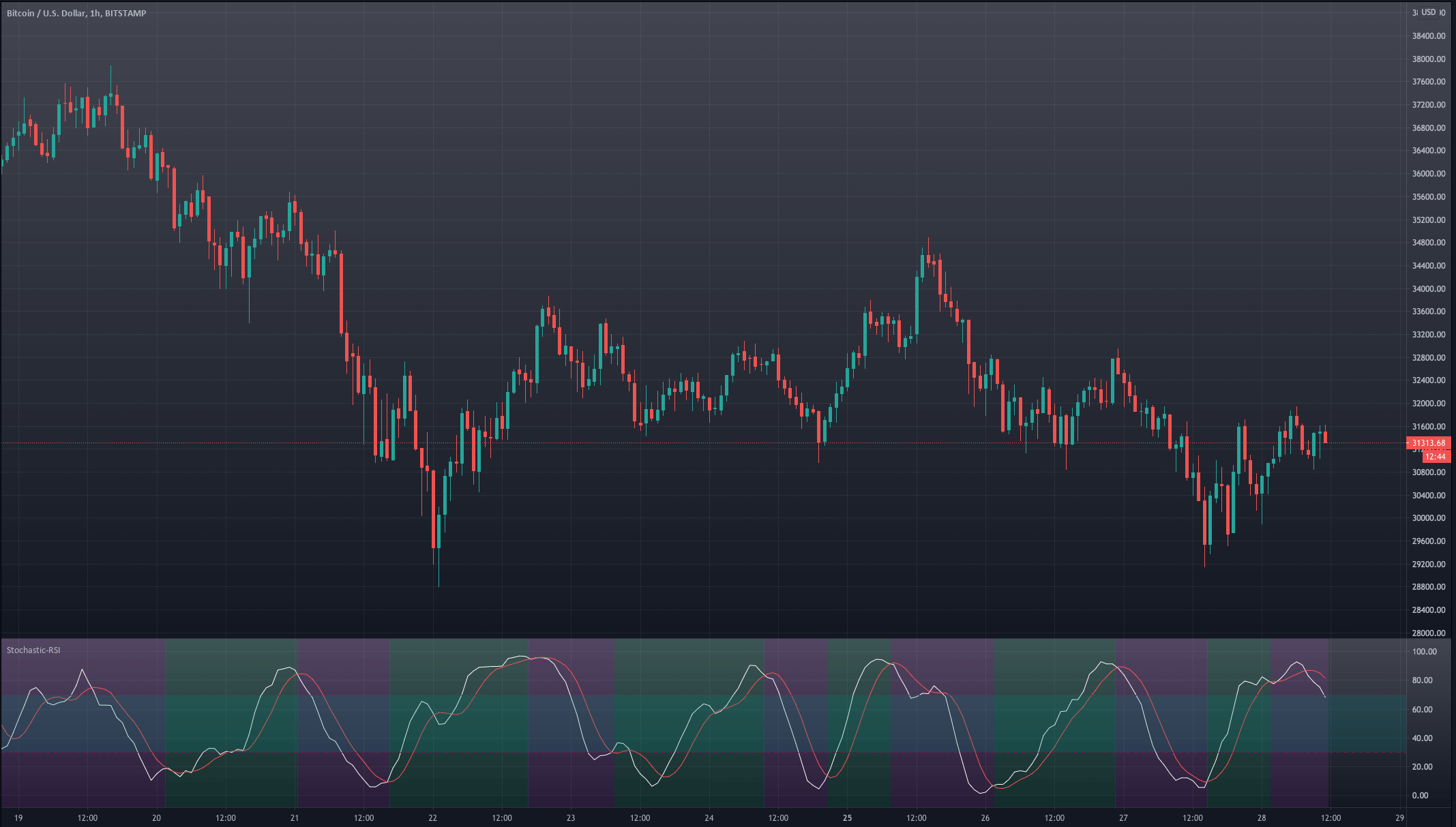

Let’s see how it behaves in the chart.

Variant 2 is an improvement. We see that the bull and bear phases match the actual movements of the market, although entries are still a bit early, and in some cases, it missed the right direction. It can be useful as a trigger signal, provided we can filter out the faulty signals.

Variant 3 – the transition occurs when d moved to the overbought or oversold region and, later, crosses to the mid-area.

Bull: the d-line crosses over the os-line

Bear: the d-line crosses under the ob-line.

if crossover (d, os)

SRSI_Long := true

SRSI_Short := false

else if crossunder (d, ob)

SRSI_Long := false

SRSI_Short := true

else

SRSI_Long := SRSI_Long[1]

SRSI_Short := SRSI_Short[1]

// bacground color change

bgcolor(SRSI_Long ? color.green: na)

bgcolor(SRSI_Short ? color.red: na)

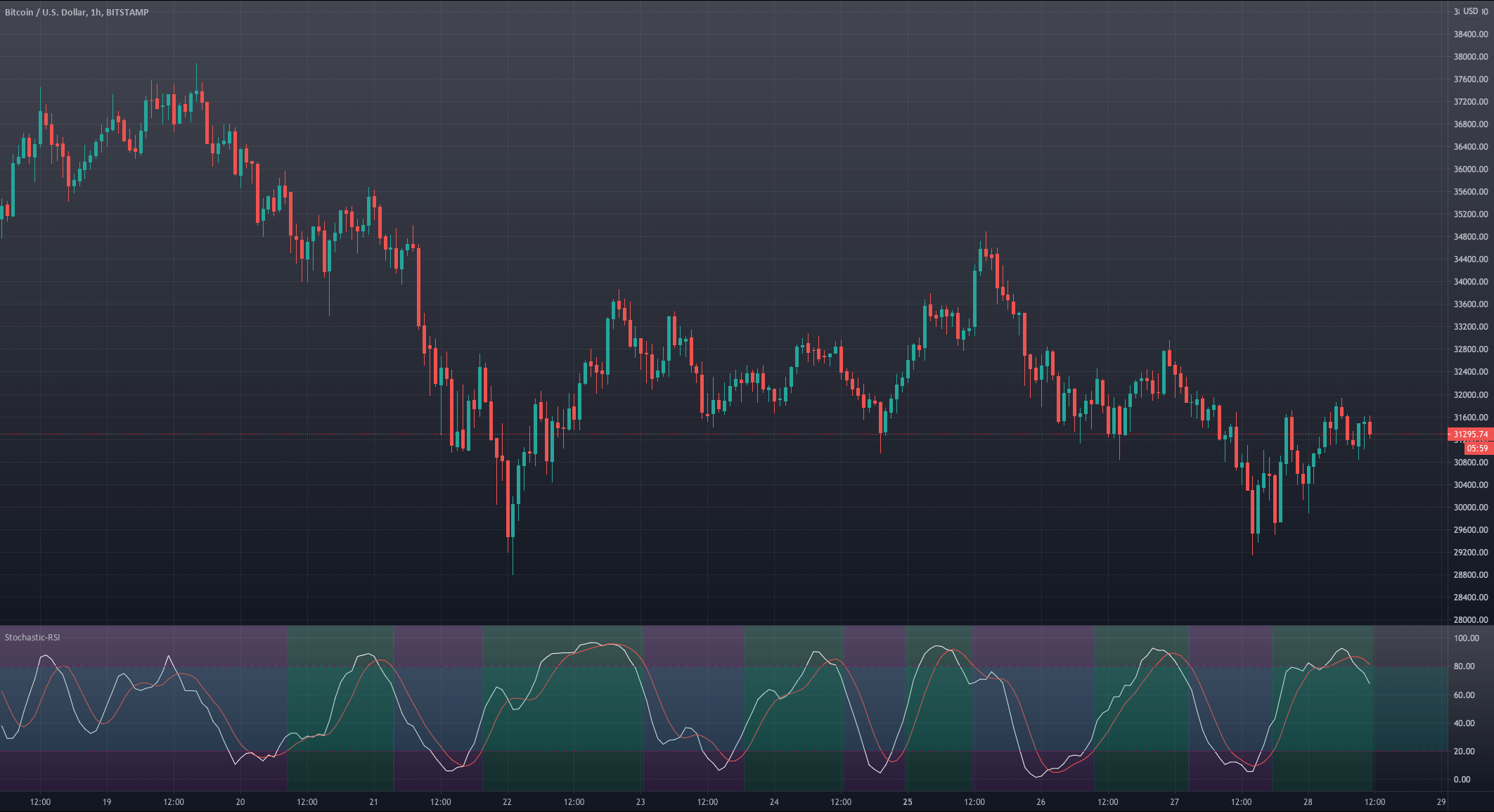

And this is how it behaves in the chart.

Variant 3 lags the turning points slightly, but this quality makes it more robust, as, on most occasions, it’s right about the market direction. This signal, combined with the right take-profit, may create a high-probability trade strategy.

Let’s try this one. But this will be resolved in our next and last article of this series.

Stay tuned!