Have you ever considered how to use volatility in your trading? How to apply some filters according to their behavior? The ATR indicator can help you with this. In this article you will be able to show you a lot of information about the Average True Range (ATR), an indicator unfairly forgotten in trading systems.

Index

- What are technical indicators and how can I use them?

- What is the ATR?

- How did ATR come about?

- How to calculate the ATR – Average True Range

- Find true range (True range)

- Calculation of the ATR indicator

- Graphic representation of the Average True Range

- Uses of ATR

- More frequent strategies using ATR

- Momentum strategies

- Böllinger bands

- Supports and resistors

- Conclusion

What are technical indicators and how can I use them?

The technical indicators, among those found in Average True Range (ATR) is based on a series of calculations on price action (some also on volume). I am sorry to say that the use of technical indicators does not always work. But they can be useful tools for detecting patterns of market entry and exit.

There are a number of technical indicators that have been developed, some show us when the market enters an overbought or oversold situation, others show us when a trend can be exhausted, if a movement is reliable and how much travel it can have.

The ATC shows us the volatility in a market, as well as its variations.

What is the ATR?

ATR stands for the name of this technical indicator: Average True Range. This indicator was developed by J. Welles Wilder. It is no more than an average of the price ranges (in fact, its name in Spanish corresponds to the average of the true range). A true range is the measure of volatility that can exist between two successive time periods (for example, two stock market sessions, two weeks, two hours, etc.).

To the point, it is a technical indicator of volatility. Volatility shows the strength they have, have had and can have (based on estimates) price movements. This can be useful both to calculate the risk and to filter market entries and exits (later we will delve into the importance of all this for our trading). The ATC simply reflects the periods in which the market has behaved more violently (is more volatile) and whether volatility increases or decreases.

How did ATR come about?

Wilder, the creator of this and other technical indicators (such as the Relative Strength Index; RSI or the Parabolic SAR, among others), was a commodity market operator. This trader used financial futures for its operations. Futures are leveraged instruments (like trading with Forex and CFDs) and are therefore very sensitive to strong price movements. For this reason, he discovered that it would be useful to have a tool that would allow him to know the range in which the market can move in a day.

However, it may be that the market opens at a different price than the previous session (what is known as a gap or gap) and does not move much further during the present day. In this case, the behavior in a day is not very volatile, but if we take into account the variation with respect to the previous closure, in fact, there may have been volatility.

For this reason, Wilder developed a calculation formula that allowed not only to see the volatility of a single day but in contrast to the previous day. Similarly, by averaging this calculation, you can observe how volatility in the market evolves over a period of time. His idea, which remains in force, was that after a period of high volatility he was continued from a period of low volatility; and vice versa.

All the technical indicators developed by J. Welles Wilder can be found in his book “News Concepts in Technical Trading Systems” (1978).

How to calculate the ATR – Average True Range

Like all other technical indicators, the Average True Range (ATR) is based on calculations of past price movements. To calculate this volatility indicator we must start from the True Range of the current period (True Range). The periods to be taken as the basis for the calculation (i.e., the number of immediately preceding sails or rods taken into account) must also be configured.

As a general rule, the period used is 14 (can be daily, weekly or monthly periods). Wilder, its creator, used this value for its development (in addition, on a daily basis). However, there are traders who use a very different trade from the father of the ATR and for this reason, the period is configurable.

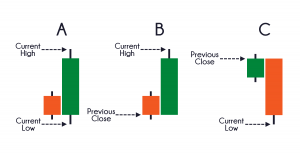

Find true range (True range)

As I mentioned before, the ATR indicator is only an average of the true range calculated over the periods indicated. It is taken as a value to define the range (True Range), the highest value of these three:

- The maximum price for the current period – minimum price for the current period.

- The maximum price for the current period – closure of the previous period.

- Previous period closure – the minimum price for the current period.

The difference between prices (in other words, the range of movement they have had) shows whether the market has been more or less volatile. The higher the range means the more volatility there has been.

Thus, the true range includes gaps that may arise in a market. This price difference, by taking the stock exchange session, better reflects the strength of the swings and helps us measure volatility in a more reliable way. As a last point, when creating an average on these values, we can observe the volatility changes. In other words, whether it goes up or down.

Calculation of the ATR indicator

The formula for calculating the ATR indicator is as follows:

ATR= [(previous ATR * n-1) + True range of the current period]/n

Wherein is the current period.

In any case, the default configuration of the ATR, which Wilder left us, was done over a period of 14 days. As discussed above, periods are taken on a daily basis (i.e., to calculate the ATR we take the price movements from the previous 14 sessions).

Thus, the original ATR would read as follows:

ATR= [(ATR previous period *13) + True range of current period] /14

Although this is the formula that its creator used to operate in the commodity market and know its volatility, the ATR can be configured according to the market, your trading style (scalping, swing, etc.), or strategy that you can use.

Graphic representation of the Average True Range

To make it easier to use the ATR indicator, it is graphically displayed at the bottom of our quotation chart (although there are platforms that allow you to place it at the top). The vast majority of trading platforms have this indicator and you just have to select it in the corresponding section and insert it. They also allow configuring of the number of periods on which we want to do the calculation. The ATR is represented by a linear graph, in which you can see the peaks and valleys of volatility. Increases and decreases in value are seen at a glance.

Uses of ATR

ATR has different uses in our trading. It can be useful both in designing strategies and in calibrating risk. As I mentioned at the beginning of this article is one of the most useful technical indicators, but, curiously, the least used.

Some of the uses we can give the Average True Range (ATR) are:

To calculate the size of the position in our trading account: dividing our risk according to the existing volatility (taken as a multiple of the ATR), we are in a position to limit the size of our trade.

Define the stop loss level: this is one of the most widespread uses of the ATR indicator. Sometimes you don’t know if the stop-loss order is too close to the price. Volatility can give you the answer. Knowing the violence with which the financial asset can move, we can calculate a safety margin to place our stop.

Set profit targets: just as we can limit risk based on the potential range of price movements. The ATR indicator will be useful to determine how far a movement has traveled. This way we will have an idea of what we can gain with an operation and set our take profit order.

To create strategies based on breaks: when the price goes through a trend, a channel, support or resistance, we must ask ourselves is this break reliable? If the price breaks with force, that is, with an increase in volatility, the break is more likely to be valid.

Select assets to trade: with the ATR you can create a filter to select which assets to trade on. You may want to exclude those in which volatility has been low and an explosion in price is expected. Assets that have excessive or very low volatility can also be discarded. To be able to compare the volatility of the assets, you just have to divide the ATR by its price and get a percentage (multiply it by 100).

More frequent strategies using ATR

Another of the most common uses of ATR is to use it as a criterion or filter within our trading system. For example, we can define that market entries occur “when volatility is greater than… (Usually a multiple of the ATR is taken).

Momentum Strategies

The ATC may indicate a change in the direction of prices. Bullish trends tend to occur in a less volatile way than market declines. If it is applied in an uptrend (in the long run) and there is an increase in volatility, it is possible that there will be a possible increase in panic and, therefore, a change in the direction of prices. Similarly, it is possible to exploit a bearish trend that is ending if we observe a decrease in volatility.

Böllinger Bands

A trading system could be, for example, combining the ATR with Böllinger Bands. If the price reaches the upper band and there is an increase in volatility, it is possible that we are facing a variation.

On the contrary, given that price falls occur with greater volatility, when the price reaches the bottom band and there is a decrease in the price, it could be interpreted as the end of the decline. As always this should be seen through a backtest. But I can tell you already that some of my strategies use ATR as an entry and exit criterion.

Supports and Resistors

This strategy has been outlined above when discussing the uses of ATR. However, it should be recalled that a strong price movement is more reliable as it better reflects market sentiment. The ruptures of supports and resistances must be validated and this indicator can help us to confirm it.

Conclusion

As you will have seen, the ATR (Average True Range) is a complete technical indicator that can be useful to exploit inefficiencies or improve your trading systems. Volatility is one of the most important aspects of the market and should be taken into account in your strategies. The ATR indicator can be incorporated into other systems and strategies. But it can also be an important element in determining risk and establishing proper risk management.