If you’re new to the forex trading world, you might find yourself scratching your head at some of the terminologies. Terms like leverage, broker, and pip often confuse beginners, but it’s easy to understand these terms if you spend time researching what they mean. Today, we will start by discussing the common trading term “lot”, which simply refers to the size of a trade or the amount that the trader is trading at any given time.

There are four different lot sizes:

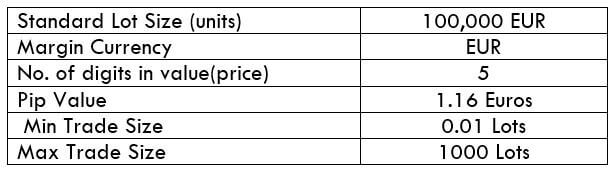

- A Standard lot is equal to 100,000 units of the base currency

- A Mini lot is equal to 10,000 units of the base currency or 10% of the standard lot

- A Micro lot is equal to 1,000 units of the base currency or 1% of the standard lot

- A Nano lot is equal to 1,000 units of the base currency or 0.1% of the standard lot

A standard lot is often considered to be the default lot size, but many brokers offer accounts that support the trading of mini and micro lots. It’s a bit harder to find an account that supports nano lots, although this isn’t impossible.

For example: If you trade 1 lot (100,000 units) of AUDUSD, the size of your trade is equal to 100,000 units of the AUD currency.

What is a Pip? Understanding Pips and their Value

We mentioned the term “pip” earlier as another trading term that leaves many beginners feeling confused. A pip, also known as a percentage point, refers to the change in value between two different currencies. With the exception of yen pairs, a pip is typically 0.0001. With yen currencies, a pip is 0.01.

For example: If the value of EURUSD opens at 1.1465, and closes at 1.1475, the difference in value is 10 pips.

Traders use this formula to calculate the value per pip:

Pip value in Counter/Quote currency = (pip in decimal X 100,000)

If you’re still confused, you don’t have to worry about calculating pip value manually, as you can simply use a free pip value calculator online. It’s important to understand why pip value is needed because traders need to know about lots, pips, and pip value in order to calculate their profits and losses. In order to do so, you’ll use this formula:

Profit/Loss = Number of Pips x Value per Pip x Lot size

Example 1: You buy Euros at $1.2178 per Euro and sell at $1.2188 per Euro with a transaction size of 100,000 (one standard lot). In order to calculate your profit or loss, you’ll plug the numbers into the provided formula:

(1.2188 – 1.2178) X 100,000 = $100

In this example, we subtracted the buying price from the selling price and then multiplied by the transaction size of 100,000 (one standard lot). The result shows that there was a $100 profit from this transaction.

Example 2: You buy GBP at 1.8384 and sell at 1.8389 with a transaction size of 10,000 (one mini lot). You’ll then plug these numbers into the formula:

(1.8389 – 1.8384) X 10,000 = $5

In this example, the transaction produced a $5 profit. Note that we multiplied by 10,000 because the size of the transaction was one mini lot, while we multiplied by 100,000 in the first example because the size was one standard lot.

Using a Position Size Calculator

As we mentioned earlier, you can find a free position size calculator online if you’d prefer to avoid manual calculations. A quick Google search for “forex position size calculator” will bring up several results. From there, you’ll just need to plug the details into the calculator and sit back while it does the work for you.